U.S. Mortgage Market Holds Firm — 30-Year Rates Hover Around 6.2 %

As of early December 2025, the U.S. mortgage market remains in a state of cautious stabilization. The current mortgage rates for a 30-year fixed loan settle around 6.26–6.32 percent, giving homebuyers and refinancers a moment of comparative calm.

The average on a 15-year fixed mortgage stays lower, offering slightly more manageable payments — though overall borrowing costs remain elevated compared with historical norms.

Meanwhile, for borrowers eligible for veterans loans, the current VA mortgage rates track somewhat differently. Depending on the lender and loan structure, 30-year VA mortgage interest can diverge from standard conventional fixed rates.

What’s Driving the Current Mortgage Climate

Several factors converge to shape today’s mortgage rate environment. At the macro level, investor demand for safe assets — particularly 10-year Treasury bonds — exerts pressure on long-term interest rates. When demand for Treasuries rises, yields tend to drop, which can nudge mortgage rates downward.

Still, uncertainty looms. Economic indicators such as inflation, government fiscal policies, and global market volatility discourage large downward swings in rates. Lenders themselves remain cautious: while some advertise competitive rates, actual offers depend heavily on a borrower’s credit profile, down payment, and loan-to-value ratio.

On the refinancing front, mortgage refinance rates remain slightly elevated relative to the lowest rates in recent memory — although they have softened compared with peaks earlier in the year. That has tempered enthusiasm among homeowners considering refinancing their existing mortgages.

Credit Conditions, Borrower Profiles, and Mortgage Loans

When lenders evaluate applications for mortgage loans — whether purchase or refinance — they weigh a variety of borrower-specific factors. Among them: credit score, debt-to-income ratio, down payment size, and the loan amount relative to property value. As a result, advertised rates for 30-year fixed or VA loans often differ from the “as-low-as” rates consumers see on rate-quote websites.

Because of these variables, not everyone qualifies for the “best current mortgage rates.” The reality is that many borrowers end up with higher interest rates or less favorable loan terms — especially if their credit profile or down payment is below lender expectations.

That dynamic underlines why it remains important for potential borrowers to shop carefully. Comparing multiple offers and understanding each lender’s underwriting criteria can make a major difference in long-term costs.

2025 Trends: A Year of Fluctuation, With Some Late Relief

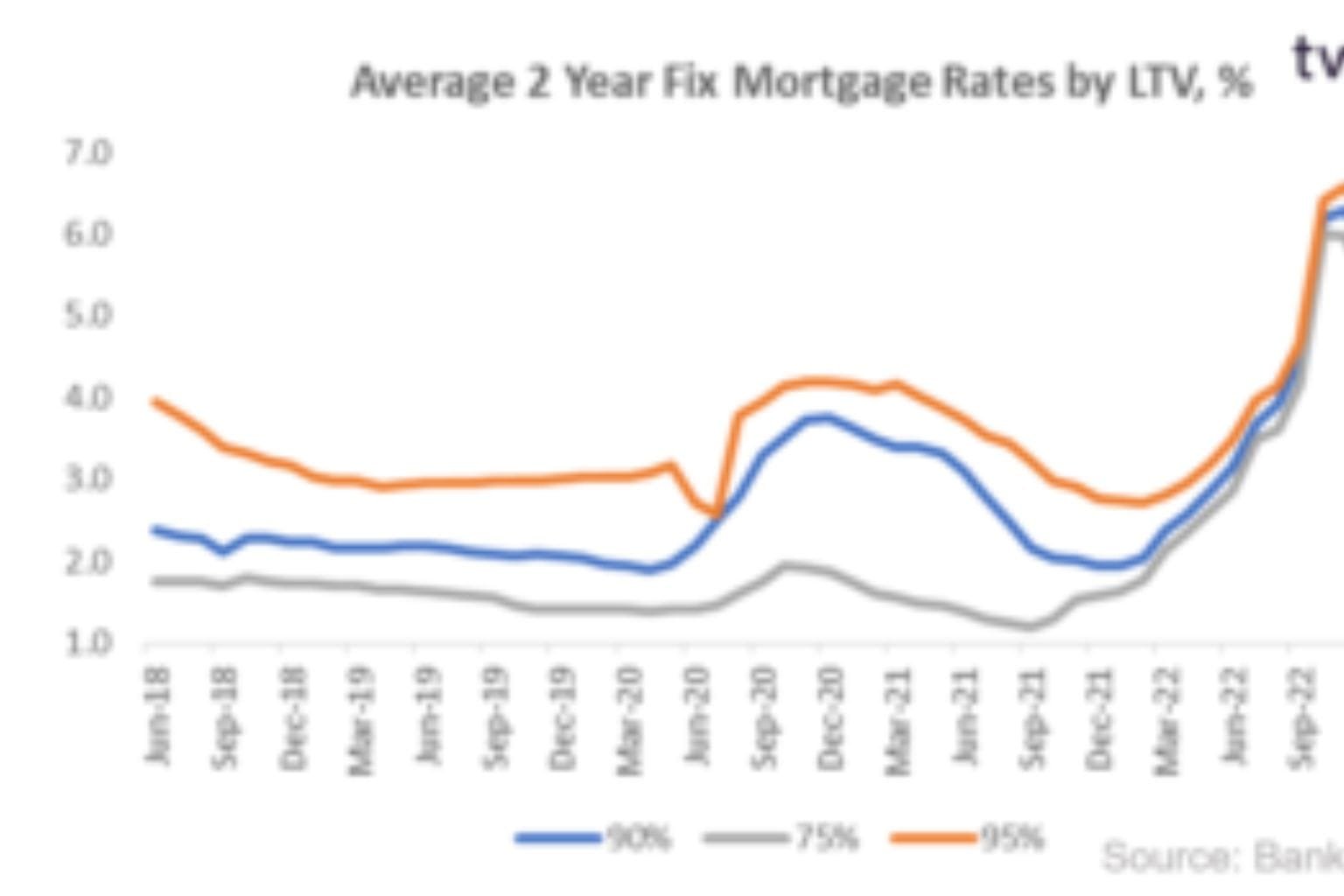

The year 2025 brought volatility for the mortgage market. For much of the year, average 30-year fixed-rate mortgages stayed near roughly 6.7%, well above the long-term average.

But beginning in the fall, a series of economic signals — including potential rate cuts by the central bank and shifting investor behavior — produced a modest downward trend. By early December, some rate surveys showed 30-year fixed rates around 6.19–6.25%.

Still, volatility persists. Weekly fluctuations remain common, and lenders continue to factor in risk premiums tied to inflation uncertainty and market instability. That dynamic weakens the odds of a sustained plunge in mortgage costs — at least for the moment.

What This Means for Homebuyers, Refinancers, and VA Borrowers

For Homebuyers

If you’re in the market for a new home, the current environment offers a somewhat stable backdrop — but the cost of financing remains high compared with historical norms. Locking in a 30-year mortgage at around 6.26 % could still make sense, especially if home prices remain elevated and you expect interest rates to stay flat or climb.

Before committing, carefully review your down payment plan, credit profile, and long-term financial forecast. Lenders may offer different mortgage loans with varying terms.

For Those Considering Mortgage Refinance

Refinancing can reduce monthly payments or shorten loan durations — but with refinance rates still elevated, the savings may be limited. Compare current rates against your existing loan’s terms. If the difference doesn’t justify closing costs and fees, it may not be worth refinancing now.

For borrowers with strong credit and enough equity in their initial loan, refinancing might still pay off. But expect lenders to evaluate applications tightly.

For VA Loan Applicants

Borrowers eligible for VA loans should pay particular attention to both standard and VA-specific rates. The current VA mortgage rates sometimes diverge from conventional fixed rates. Lenders offering VA loans may provide competitive terms — but qualification criteria (credit history, service record, etc.) still apply.

If you qualify, a VA loan may offer benefits like lower down payment, more flexible underwriting, or favorable refinance terms.

Outlook: What to Watch in the Next Few Months

Economists and market watchers expect that mortgage rates will remain somewhat elevated in the near term. Unless there is a sharp drop in inflation or a shift in investor sentiment, rates are unlikely to return to historically low levels.

On the other hand, if the financial markets stabilize, and if central bank policy becomes more dovish, there remains a possibility of modest softening in mortgage refinance and purchase rates. That could present a window of opportunity for borrowers with solid profiles.

For now, borrowers and homebuyers should carefully monitor current mortgage rates chart trends, compare offers from different lenders, and pay attention to their own financial readiness before locking in a mortgage.

FAQ – Current Mortgage Rates & Market Updates

1. What are the current mortgage rates right now?

Current mortgage rates hover near 6.2% to 6.3% for a 30-year fixed loan. Rates vary depending on lender, credit score, and loan type.

2. Are mortgage refinance rates lower than purchase rates?

Refinance rates are often slightly higher than purchase rates, depending on market demand and lender risk assessments.

3. How do I find the best current mortgage rates?

Compare quotes from multiple lenders, maintain a strong credit profile, and review updated rate surveys from reputable sites like Bankrate and Mortgage News Daily.

4. Are current VA mortgage rates different from conventional rates?

Yes. VA mortgage rates can be lower because VA loans include government-backed benefits for eligible veterans and service members.

🚀 Power Up Your Digital Presence with RojrzTech

Your business deserves technology that moves fast, performs strong, and keeps you ahead of the competition. At RojrzTech, we build digital solutions that help brands grow smarter—from website development and smart automation to marketing systems that actually deliver results.

Whether you’re aiming for higher visibility, stronger engagement, or next-level digital performance, our team is ready to help you take the next step.

📩 Let’s Build Something Game-Changing.

Connect with RojrzTech today and unlock the future of your brand.